Welcome to ILSR's complete library of resources and publications. Use the filtering tools below to find just the content you're seeking, or subscribe to the RSS feed here.

Powering a Political Revolution, North Dakota’s Non-Partisan League (Episode 4)

In this episode, Chris Mitchell, the director of our Community Broadband Networks initiative, interviews David Morris, the co-founder of the Institute for Local Self-Reliance and...

In this episode of the Building Local Power podcast, our guest is Justin Dahlheimer, president of a community bank in west-central Minnesota. Justin and our...

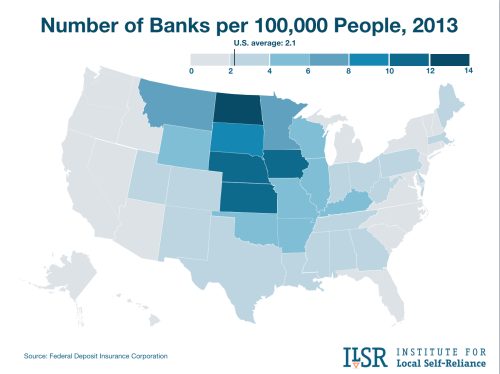

Report: Fewer Small Businesses are Receiving Federal Relief Loans in States Dominated by Big Banks

A significantly larger number of federal relief loans are reaching small businesses in states where small, local banks comprise a greater share of the market.

In this cover story for Sojourners Magazine, Stacy Mitchell writes that there is remarkably little evidence to support the idea that bigger banks are superior.

“Trustbusting Is Making a Comeback”: Stacy Mitchell’s Keynote at the National Rural Grocery Summit:

Stacy Mitchell's barnburner keynote address at the National Rural Grocery Summit detailed how monopolistic corporations are harming small businesses and farmers.